For the first time, no Codelco operation appears on the list.

By Patricia Marchetti.

At the height of the historic copper price rally and amid El Teniente’s decline, only two Chilean mines rank among the world’s top 10, whereas a decade ago Chile accounted for half of the list.

Copper is currently experiencing what seems to be an unstoppable boom. Following a string of record-breaking prices — which have climbed even further in 2026 — the metal that is essential for the energy transition has surpassed US$6.6 per pound, driven by expectations of rising demand from artificial intelligence and persistent supply constraints. In fact, due to the disruptions caused by the war in the Middle East, analysts have once again forecast a copper market deficit for 2026.

In this context, Chile continues to hold its position as the world’s largest producer, accounting for 23% of global copper output, which reached 23.1 million tonnes last year.

However, when looking at the ranking of the world’s largest copper mines, the country has been steadily losing representation and, for the first time in history, none of Codelco’s mines appear on the list.

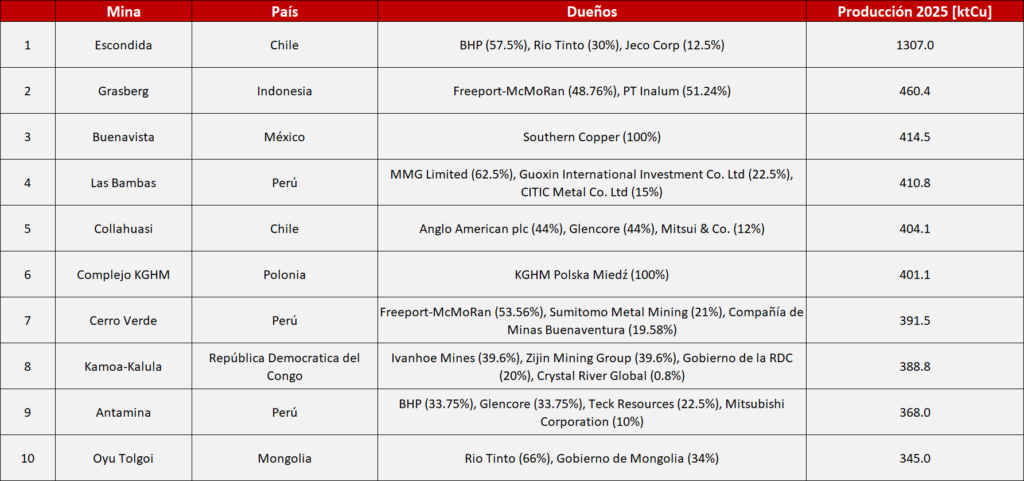

According to an analysis conducted by consulting firm Plusmining for DF, the undisputed leader among the world’s largest copper deposits is Chile’s Escondida mine, which produced 1.3 million tonnes of copper in 2025.

This annual figure is not only BHP’s best operational performance since 2007, but also the main reason why the Australian mining giant now refers to itself as “the world’s largest copper producer,” since this single operation outperformed all seven divisions of the Chilean state-owned company, historically the industry leader.

The only other Chilean mine on the list is Collahuasi, which ranks fifth with 406,000 tonnes of copper, despite this being its weakest production result since 2012.

The Great Absentee: Codelco

“The departure of Codelco’s divisions from the global Top 10 — where Radomiro Tomic, Chuquicamata, and until last year El Teniente had historically appeared — is a critical symptom of the production stagnation affecting the state- wned company,” says Juan José Pardo, Mining Industry Analyst at Plusmining.

“This phenomenon reflects the complex situation surrounding the structural projects,” he adds, referring to Chuquicamata Underground and El Teniente’s New Mine Level project, which have failed to ramp up quickly enough to offset declining ore grades at these deposits, both of which have more than 100 years of operating history.

Added to this are geomechanical and geotechnical challenges, especially at El Teniente, Pardo explains, where rock bursts have forced the shutdown of key sectors, including the accident last year that resulted in a 13% decline in production at the world’s largest underground copper mine.

Meanwhile, Gustavo Lagos, professor and mining expert at the Pontifical Catholic University of Chile (PUC), says it is “expected” that Codelco’s mines have dropped out of the Top 10 due to the sharp decline in their production over the past 20 years. In the specific case of Chuquicamata, he notes that output “fell from more than 650,000 tonnes in 2005 to 265,000 tonnes in 2025 due to the depletion of the open-pit mine and, from 2019 onward, the start-up of the underground operation, which produced far less than expected because of massive collapses in 2020 and subsequent years.”

Currently, El Teniente would rank 12th in the global ranking, while Chuquicamata would place 14th.

Largest Copper Mines 2016

Source Plusmining

Largest Copper Mines 2025

Source Plusmining

Chile Loses Ground

It is not only Codelco. The current picture of the world’s largest copper mines is very different from that of 10 years ago, when half of the top-ranked operations were Chilean: Escondida (1), Collahuasi (2), El Teniente (5), Los Pelambres (9), and Radomiro Tomic (10). At that time, Los Bronces and Chuquicamata were also close behind.

Pardo emphasizes that “Chile maintains global leadership thanks to its aggregate production volume, but the presence of only two operations in the Top 10 reflects structural exhaustion in the face of increasingly dynamic global competition.” He explains that “while mining projects in Chile are mostly brownfield operations struggling with an average ore grade of 0.60%, the Democratic Republic of Congo has emerged with greenfield deposits such as Kamoa- Kakula, whose 2.82% ore grade is nearly five times higher.”

Indeed, thanks to these exceptionally high grades, the Central African country has tripled its copper production over the last decade, positioning itself today as the world’s second-largest producer.

“The rise of Africa, together with new projects coming online in Russia and Peru, shows that the competitive gap is narrowing due to the maturity and growing operational complexity of Chile’s mining portfolio compared to younger and richer mining districts,” adds the Plusmining expert.

Source: Diario Financiero